.png?width=505&height=89&name=GVC%20Mortgage%20(4).png "GVC Mortgage (4)")

What You Need to Know About Contributing to Your IRA

Everyone wants a retirement where they can relax, not worry about finances, and still be able to do the things they’ve always wanted to.

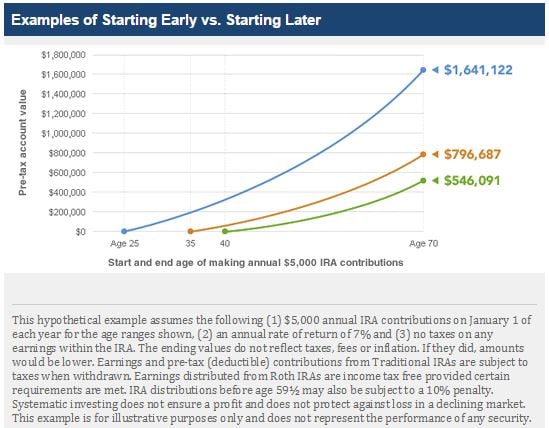

Whether you’re 22 and just starting your career or you’re 35 and have a few years under your belt, it’s never too late to start saving for your comfy retirement by contributing to your individual retirement account (IRA).

Image by Fidelity

Making contributions can be tricky if you don’t know all the rules. Here’s a brief overview of what you need to know about contributing to your IRA.

Choosing the right IRA for you

Perhaps the best place to start is to determine what type of IRA will suit you best. When deciding between a traditional IRA and a Roth IRA, you must consider your current tax bracket and what tax bracket you anticipate you’ll be in during your retirement.

This decision may seem difficult because you can only plan so far in advance. Just remember you can always transfer funds or open an additional account later.

|

|

|

|

|---|---|---|

| Contribution type |

|

|

| Max Contribution (for 2014 & 2015) |

|

|

| Contribution Deadlines |

|

|

| Contribution Age Limit |

|

|

| Withdrawal |

|

|

| Minimum Distributions |

|

|

Consolidating your accounts

If you currently have multiple IRAs or 401ks from more than one employer you can consolidate those into one account, or at least under one financial institution, which should help you manage your money more efficiently. In fact, more than 10 times as many dollars are added to IRAs through rollovers than through direct contributions.

Asking for help

Saving for retirement can seem confusing and this list is in no way all inclusive of what you need to know before you start contributing to your IRA. To clear up any confusion about the technicalities associated with IRAs, and to make the most of your contributions, be sure to talk to a financial advisor.

How are you saving for your retirement?

.png)